When you hear “open banking,” it might sound technical or invasive—but it’s simply a new way for banks to let customers securely share their financial data with third-party services. Open banking makes your personal accounts more interoperable, paving the way for smarter apps and more user control.

What Open Banking Means

Open banking uses secure APIs to let third-party providers (with your permission) access your financial data—such as account balances, transaction history, and payment capabilities. Unlike sharing passwords, APIs enable controlled and audited data sharing.

How It Works

API access replaces screen scraping.

You can authorize apps to read data or initiate payments.

Banks log these requests, ensuring transparency and consent.

Why It Matters

For consumers: Get smarter budgeting tools, easier loan applications, and more seamless money management.

For businesses: Build richer financial products (e.g., tools that auto-categorize expenses, forecast cash flow).

For banks: Shift to providing tools and analytics rather than just storing money.

Real-World Example

Citizens Bank launched a secure open banking API in March 2025. It helped cut screen scraping by 95%, boosting security and enabling real-time invoicing and financial planning tools blog.genome.eubusinessinsider.com.

Challenges & the Road Ahead

Privacy concerns: Who else can access or monetize your data?

Regulation: Europe and the UK led the charge; the US is behind but catching up.

Scope expansion: Look out for APIs enabling investment, mortgage, and insurance data in the future.

Final Thoughts:

Open banking is transforming finance by putting control in the hands of consumers and enabling innovation through data sharing. As regulations evolve and more banks join in, expect richer, smarter services across the board.

Hedge funds are private investment vehicles that use a variety of strategies to generate high returns for their investors. Unlike mutual funds or exchange-traded funds (ETFs), hedge funds often take aggressive approaches, including short selling, leverage, and derivatives trading. They are typically available only to accredited investors due to their high risk and significant minimum investment requirements.

How Hedge Funds Work

Hedge funds pool money from investors and are managed by professionals who have the flexibility to invest in a wide range of asset classes, such as stocks, bonds, commodities, real estate, and even cryptocurrencies. Their goal is to deliver high returns, regardless of whether the market is going up or down.

Hedge funds differ from traditional investment funds because they are less regulated. This allows fund managers to use complex strategies that might not be permitted in mutual funds or ETFs.

(Image suggestion: A flowchart showing how hedge funds collect investor money and allocate it across different assets.)

Common Hedge Fund Strategies

Hedge funds use various strategies to maximize returns. Some of the most common include:

Long/Short Equity: Buying stocks expected to rise while short-selling stocks expected to fall.

Market Neutral: Balancing long and short positions to reduce market exposure.

Global Macro: Investing based on large-scale economic trends, such as currency movements and interest rates.

Event-Driven: Profiting from corporate events like mergers, bankruptcies, or restructurings.

Distressed Assets: Buying securities from struggling companies at a discount, hoping for recovery.

Each strategy has its own risk level and potential for returns. Some hedge funds specialize in just one approach, while others combine multiple strategies.

(Image suggestion: A table listing these strategies with brief descriptions.)

How Hedge Funds Make Money

Hedge funds operate under a “2 and 20” fee structure, meaning they charge:

2% management fee: A percentage of the total assets under management (AUM), paid annually.

20% performance fee: A percentage of the fund’s profits, incentivizing managers to deliver strong returns.

For example, if a hedge fund manages $1 billion and generates a 10% return ($100 million), the fund manager earns $20 million in performance fees, plus $20 million in management fees (2% of $1 billion).

While this structure rewards high performance, it has been criticized for being costly, especially if the fund underperforms.

(Image suggestion: A simple breakdown of the “2 and 20” fee structure in a graphic.)

Pros and Cons of Hedge Funds

Pros

Potential for high returns

Flexibility to invest in diverse assets

Can generate profits in both rising and falling markets

Cons

High fees compared to other investment options

Often require large minimum investments

Can be highly risky and volatile

(Image suggestion: A side-by-side comparison of hedge fund pros and cons.)

Should You Invest in a Hedge Fund?

Hedge funds are best suited for wealthy, risk-tolerant investors who can afford to lock up their money for extended periods. If you are considering investing in a hedge fund, make sure you understand the strategy, risks, and fee structure before committing.

For most everyday investors, mutual funds or ETFs may offer a more accessible and cost-effective way to achieve diversified investment exposure.

(Image suggestion: A decision tree or flowchart helping readers determine if hedge funds are right for them.)

Conclusion

Hedge funds are complex investment vehicles designed to maximize returns through unique and often risky strategies. While they offer opportunities for high profits, they also come with steep fees and potential losses. Understanding how hedge funds operate can help investors determine whether they are a good fit for their financial goals.

Banking has evolved rapidly in the digital age. While traditional banks have long dominated the financial landscape, a new wave of digital-only financial institutions—known as neo-banks—has emerged and gained popularity, especially among younger, tech-savvy users. But what exactly sets them apart?

This blog explores the differences between neo-banks and traditional banks, including how they work, what they offer, and which might suit your needs best.

What Are Traditional Banks?

Traditional banks are the well-known brick-and-mortar institutions that have been around for decades, such as JPMorgan Chase, Bank of America, Wells Fargo, and Citibank.

Key Features:

Physical branches and ATMs

Full-service offerings including checking, savings, credit cards, mortgages, and investment services

Heavily regulated by federal and state authorities

Typically offer FDIC insurance (up to $250,000 per depositor)

Advantages:

In-person support

Long-established trust and reputation

Wide range of financial products and services

Access to physical cash and teller services

Limitations:

Often charge higher fees

Slower innovation

May require in-person visits for certain services

What Are Neo-Banks?

Neo-banks (also known as digital banks or challenger banks) operate entirely online. They do not have physical branches and rely on mobile apps and web platforms to offer streamlined banking services.

Examples include Chime, Revolut, N26, and Monzo.

Key Features:

Digital-only platforms

Focus on low fees, user experience, and convenience

Often partner with licensed banks to offer FDIC insurance

Quick account setup and real-time spending notifications

Advantages:

Easy and fast sign-up process

Low or no monthly fees

Innovative tools like budgeting, savings automation, and instant alerts

Strong mobile user experience

Limitations:

No physical locations

Limited product range (often no loans or mortgages)

Customer service may be slower or app-only

May lack the deep financial stability and security history of legacy banks

Comparing the Two: Side by Side

Feature

Traditional Banks

Neo-Banks

Physical Branches

Yes

No

Fees

Often higher

Usually low or none

FDIC Insurance

Yes (direct)

Yes (via partner banks)

Product Variety

Extensive

Limited

Customer Support

In-person and online

Online or in-app only

Speed of Innovation

Slower

Fast and tech-focused

Who Should Choose a Traditional Bank?

People who prefer in-person service

Customers with complex financial needs (mortgages, wealth management, business loans)

Those who rely on services like cashier’s checks or safe deposit boxes

Who Should Choose a Neo-Bank?

Individuals comfortable with digital tools

People looking for low-fee, straightforward banking

Frequent travelers or remote workers who don’t need branch access

Budget-conscious users wanting better financial insights through apps

The Bottom Line

Both neo-banks and traditional banks serve important roles in the financial world. The right choice depends on your personal preferences, lifestyle, and financial needs.

Neo-banks offer flexibility, lower costs, and digital convenience—ideal for those who live online. Traditional banks provide stability, face-to-face service, and a broad array of financial products.

As the banking landscape continues to evolve, many people even choose to use both, leveraging the strengths of each type to build a more flexible and effective financial strategy.

When it comes to keeping your money safe, trust in the banking system is essential. That’s where the FDIC — the Federal Deposit Insurance Corporation — comes in. Established in 1933 during the Great Depression, the FDIC was created to restore confidence in the American banking system after thousands of banks failed and people lost their life savings.

What Exactly Is the FDIC?

The FDIC is an independent U.S. government agency that protects bank depositors. Its primary role is to insure deposits in member banks, which means if your bank fails, your insured money is still safe — up to a certain limit.

It also supervises financial institutions for safety, soundness, and consumer protection, and manages receiverships when banks do fail.

How Deposit Insurance Works

The FDIC insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category(such as individual, joint, retirement, etc.). This means:

If your bank fails, the FDIC guarantees that your money — up to the limit — will be returned to you.

Coverage includes checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs).

Investment products like stocks, bonds, mutual funds, crypto, and annuities are not covered by FDIC insurance.

Example of Coverage:

If you have a savings account with $200,000 and a checking account with $30,000 at the same FDIC-insured bank, your full $230,000 would be insured.

If you have $300,000 in a single account, only $250,000 of that would be covered.

What Happens When a Bank Fails?

In the rare event that a bank shuts down, the FDIC steps in immediately. Here’s what typically happens:

The FDIC either arranges for another bank to take over the failed institution’s accounts, or

It pays depositors directly, usually within a few business days.

In most cases, insured customers regain access to their funds quickly and without hassle.

How the FDIC Is Funded

The FDIC isn’t funded by taxpayers. Instead, it collects insurance premiums from banks and savings institutions. These payments go into the Deposit Insurance Fund, which is used to reimburse depositors and manage failed banks.

This structure ensures that protection remains intact even in times of economic stress.

Why the FDIC Matters Today

Even though the banking system is much stronger today than it was in the 1930s, financial shocks can still happen — as seen during the 2008 financial crisis and more recently, with the failure of a few regional banks in 2023.

FDIC insurance helps maintain public confidence by offering a guaranteed safety net, so customers don’t feel the need to rush and withdraw funds in a panic (also known as a bank run).

How to Make Sure Your Money Is Protected

Here’s what you can do:

Make sure your bank is FDIC-insured (most banks in the U.S. are — just look for the FDIC logo or check online).

Stay aware of the $250,000 limit per account type and per bank.

Consider spreading funds across different ownership categories or institutions if your balances exceed the insurance limits.

Final Thoughts

The FDIC is a cornerstone of trust in the U.S. financial system. It quietly ensures that your money is protected — no matter what happens to your bank. By understanding how FDIC insurance works and using it to your advantage, you can make smarter, safer financial decisions.

Whether you’re just starting out with your first savings account or managing multiple financial accounts, knowing your money is insured can provide powerful peace of mind.

When you hear the term “shadow banking,” it might sound like something secretive or even illegal. But shadow banking is neither illegal nor necessarily shady — it’s simply a term used to describe financial institutions and activities that operate outside traditional banking regulations.

Unlike conventional banks, shadow banking entities don’t accept deposits or offer checking accounts. However, they perform similar financial functions, such as lending, investing, and facilitating credit flows throughout the economy.

What Counts as Shadow Banking?

Shadow banking includes a wide range of institutions and vehicles such as:

Hedge funds

Private equity firms

Money market funds

Structured investment vehicles (SIVs)

Peer-to-peer lending platforms

Certain fintech companies

These entities help connect investors to borrowers, often using complex financial instruments that don’t appear on traditional bank balance sheets.

How Shadow Banks Operate

The main role of shadow banking is credit intermediation — the process of channeling funds from savers to borrowers. They do this without the safety nets or regulations that apply to traditional banks, such as deposit insurance or central bank backing.

For example, instead of taking customer deposits, a shadow bank might raise money by selling commercial paper or asset-backed securities. This funding is then used to finance loans, investments, or other financial products.

Why Shadow Banking Exists

The shadow banking system grew rapidly in the early 2000s because it offered an alternative to the heavily regulated traditional banking sector. Shadow banks can often provide faster access to capital, invest more aggressively, and react more flexibly to market conditions.

This flexibility can encourage innovation and fuel economic growth — but it also comes with significantly more risk.

The Hidden Risks

The very things that make shadow banking attractive — lack of regulation and increased risk-taking — are also what make it potentially dangerous.

During the 2008 financial crisis, shadow banks played a major role in amplifying the downturn. Many of them relied on short-term borrowing to finance long-term investments, creating serious liquidity risks. When markets froze and investors pulled their funds, many shadow institutions collapsed, triggering a domino effect throughout the global financial system.

How It Affects the Economy Today

Even though regulations tightened after 2008, the shadow banking sector is still large — and growing. According to the Financial Stability Board (FSB), the global shadow banking system was estimated to be worth over $63 trillion.

Shadow banking supports lending and liquidity in modern markets, especially in sectors that traditional banks avoid due to risk or regulatory restrictions. However, its continued expansion remains a concern for central banks and regulators.

Key Differences from Traditional Banks

Here’s how shadow banks differ from traditional banks:

Feature

Traditional Banks

Shadow Banks

Accept Deposits

Yes

No

Regulated by Central Banks

Yes

Limited or None

Access to Central Bank Funding

Yes

No

Take On Risky Assets

Usually conservative

Often riskier

Transparency

High

Varies

Why It Matters to You

Even if you’ve never interacted directly with a shadow bank, its influence can affect your mortgage rates, the availability of credit, and the overall stability of the financial system. The 2008 crisis showed how interconnected everything is — and how a problem in shadow banking can quickly become a global issue.

Understanding how shadow banking works is crucial for anyone interested in finance, investing, or economic policy.

Final Thoughts

Shadow banking plays a major role in global finance by expanding credit availability and pushing the boundaries of innovation. However, the lack of oversight, high-risk strategies, and systemic importance of these institutions means they require close attention.

As markets evolve and traditional banking continues to face disruption from fintech and private capital, shadow banking will likely grow even more prominent — for better or worse.

Economic terms like inflation, stagflation, and hyperinflation are often discussed in financial news and analyses.Understanding these concepts is crucial, as they have significant impacts on economies and individuals alike. This article explores these three phenomena, highlighting their definitions, causes, and effects.

Inflation

Definition:

Inflation refers to the general increase in prices of goods and services in an economy over a period of time, leading to a decrease in the purchasing power of money. It is typically measured by indices such as the Consumer Price Index (CPI) or the Producer Price Index (PPI).Invexi Consulting

Causes:

Demand-Pull Inflation: Occurs when the demand for goods and services exceeds their supply, leading to price increases.

Cost-Push Inflation: Happens when production costs rise (e.g., due to increased wages or raw material prices), prompting businesses to raise prices to maintain profit margins.

Built-In Inflation: Also known as wage-price inflation, it arises when workers demand higher wages, leading to increased production costs and subsequently higher prices, creating a cycle of ongoing inflation.

Effects:

Erodes Purchasing Power: As prices rise, the real value of money decreases, meaning consumers can afford fewer goods and services with the same amount of money.

Income Redistribution: Inflation can disproportionately affect individuals on fixed incomes, as their purchasing power diminishes.

Economic Uncertainty: High and unpredictable inflation can lead to uncertainty among businesses and consumers, potentially hindering investment and savings.

Stagflation

Definition:

Stagflation is characterized by the simultaneous occurrence of stagnant economic growth, high unemployment, and high inflation. This combination presents a dilemma for policymakers, as measures to address one aspect may exacerbate another.Reuters

Causes:

Supply Shocks: Sudden increases in the cost of essential commodities (e.g., oil) can raise production costs across the economy, leading to inflation and reduced economic output.

Poor Economic Policies: Policies that excessively expand the money supply or poorly manage fiscal resources can contribute to stagflation.

Effects:

Reduced Consumer Spending: As unemployment rises and purchasing power declines, consumer spending typically decreases, further slowing economic growth.

Policy Challenges: Traditional monetary tools become less effective, as stimulating growth may worsen inflation, while controlling inflation may suppress growth further.

Historical Context:

The 1970s in the United States serve as a notable example of stagflation, where oil price shocks led to high inflation and unemployment rates, coupled with stagnant economic growth. Investopedia

Hyperinflation

Definition:

Hyperinflation describes an extremely rapid and uncontrolled increase in prices, typically exceeding 50% per month. In such scenarios, the value of currency plummets, and normal economic functions can break down. Wall Street Prep+3Investopedia+3Corporate Finance Institute+3

Causes:

Excessive Money Supply: Often results from a government printing money to finance expenditures, leading to an oversupply of currency.

Loss of Confidence: When the public loses faith in a currency’s stability, they may rush to spend it or convert it to more stable assets, accelerating price increases.NetSuite+1Investopedia+1

Effects:

Currency Collapse: Money may become virtually worthless, leading to a reliance on barter or alternative currencies.

Economic Paralysis: Businesses struggle to set prices, and consumers rush to spend money before it further devalues, disrupting normal economic activities.

Historical Examples:

Germany (1920s): Post-World War I reparations led to excessive money printing, resulting in extreme hyperinflation.

Zimbabwe (2000s): Land reform policies and economic mismanagement led to hyperinflation, with prices doubling rapidly. de.wikipedia.org

Comparative Overview

Aspect

Inflation

Stagflation

Hyperinflation

Definition

General rise in prices

Combination of high inflation, stagnant growth, and high unemployment

Extremely rapid and uncontrolled price increases

Causes

Demand-pull, cost-push, built-in factors

Supply shocks, poor economic policies

Excessive money supply, loss of confidence

Effects

Reduced purchasing power, income redistribution, economic uncertainty

Reduced consumer spending, policy challenges

Currency collapse, economic paralysis

Historical Examples

Moderate inflation in various economies

U.S. in the 1970s

Germany in the 1920s, Zimbabwe in the 2000s

Understanding the distinctions between inflation, stagflation, and hyperinflation is vital for grasping economic dynamics and their potential impacts on daily life. While inflation is a common economic phenomenon, stagflation and hyperinflation represent more severe and complex challenges that require careful policy responses to navigate effectively.

How the Federal Reserve Controls Interest Rates and Why It Matters

The Federal Reserve (Fed) plays a crucial role in managing the U.S. economy by controlling interest rates. This power influences everything from inflation and employment to mortgage rates and stock market performance. But how exactly does the Fed control interest rates, and why does it matter to businesses and individuals?

What Is the Federal Reserve and Its Role in the Economy?

The Federal Reserve is the central banking system of the United States. Established in 1913, its primary objectives are to:

Maintain price stability (control inflation)

Promote maximum employment

Ensure moderate long-term interest rates

To achieve these goals, the Fed adjusts monetary policy, mainly through interest rate control, which influences borrowing, spending, and investment across the economy.

How the Federal Reserve Controls Interest Rates

The Fed does not directly set all interest rates in the economy. Instead, it influences rates through several monetary policy tools.

The Federal Funds Rate

The federal funds rate is the interest rate at which banks lend to each other overnight. The Fed sets a target range for this rate and influences it through monetary policy tools.

When the Fed raises rates, borrowing becomes more expensive, slowing down economic activity and reducing inflation.

When the Fed lowers rates, borrowing becomes cheaper, stimulating spending and investment.

Open Market Operations (OMO)

The Fed buys or sells U.S. Treasury securities to control the money supply.

Buying securities injects money into the banking system, lowering interest rates.

This process directly affects liquidity in financial markets and influences borrowing costs for businesses and consumers.

Interest on Reserve Balances (IORB)

Banks keep reserves at the Federal Reserve. The Fed pays interest on these reserves, which sets a benchmark for short-term interest rates.

Higher reserve interest rates encourage banks to hold reserves instead of lending, reducing the money supply.

Lower reserve interest rates incentivize banks to lend more, increasing the money supply.

The Discount Rate

The discount rate is the interest rate the Fed charges banks for borrowing directly from it.

Raising the discount rate discourages banks from borrowing, tightening credit availability.

Lowering the discount rate makes borrowing easier, stimulating economic growth.

This tool is used in emergencies to provide liquidity to banks but also serves as a signal of the Fed’s policy direction.

Reserve Requirements (Rarely Used Today)

In the past, the Fed required banks to hold a certain percentage of deposits as reserves. While this tool is less commonly used today, it historically helped control the money supply.

Why Interest Rates Matter for the Economy

The Fed’s control of interest rates has widespread effects on businesses, consumers, and investors.

Impact on Inflation

Inflation occurs when prices rise due to excessive demand or supply constraints.

Higher interest rates slow inflation by making borrowing more expensive, reducing spending.

Lower interest rates can fuel inflation by increasing spending and borrowing.

Effect on Employment and Wages

Lower interest rates encourage businesses to expand, invest, and hire more workers, reducing unemployment.

Higher interest rates slow down business expansion, potentially leading to layoffs or slower wage growth.

The Fed balances interest rates to promote job growth without causing excessive inflation.

Impact on Consumer Borrowing

Interest rates affect borrowing costs for everyday people, influencing:

Mortgage rates: Higher rates make home loans more expensive, slowing down the housing market.

Car loans and credit cards: Higher rates increase monthly payments, reducing consumer spending.

Student loans: Federal student loan rates are tied to interest rate changes, affecting affordability.

Stock Market and Investment Effects

Investors watch the Fed closely because interest rates impact stock prices and market performance.

Low interest rates: Companies borrow cheaply to expand, increasing earnings and boosting stock prices.

High interest rates: Investment slows, reducing stock market gains.

Global Economic Impact

Since the U.S. dollar is a global reserve currency, Fed rate changes affect exchange rates, international trade, and investment worldwide.

Higher rates strengthen the U.S. dollar, making exports more expensive for foreign buyers.

Lower rates weaken the dollar, making U.S. exports more competitive.

Recent Trends and Considerations

As of 2025, the Fed faces complex economic conditions, balancing:

Inflation concerns after previous rate hikes.

Slower economic growth due to higher borrowing costs.

Geopolitical risks affecting global trade and supply chains.

Conclusion: Why the Fed’s Interest Rate Decisions Matter to You

Whether you are a borrower, investor, or business owner, Federal Reserve interest rate policies impact your financial future.

If you’re looking to buy a home or take out a loan, Fed decisions influence how much you’ll pay in interest.

If you’re an investor, interest rates can shape stock market trends and asset prices.

If you’re a business owner, Fed policies affect borrowing costs, expansion plans, and overall economic conditions.

Understanding how the Fed controls interest rates helps you make smarter financial decisions in a constantly changing economic landscape.

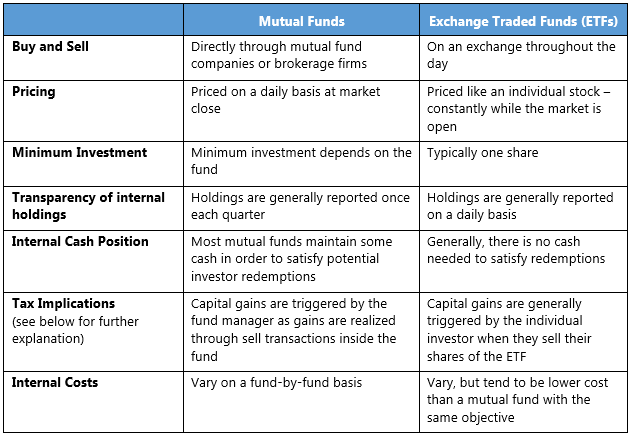

Investing offers a plethora of options, each tailored to different financial goals, risk tolerances, and investment strategies.Among the most discussed are Hedge Funds, Mutual Funds, and Exchange-Traded Funds (ETFs). Understanding the distinctions between these investment vehicles is crucial for making informed decisions.

Hedge Funds

Definition: Hedge funds are privately pooled investment funds that employ diverse and often complex strategies to achieve high returns for their investors. They are typically structured as limited partnerships or limited liability companies.Groww

Key Characteristics:

Investor Eligibility: Restricted to accredited investors, often requiring a significant minimum investment.

Regulation: Less regulated compared to mutual funds and ETFs, allowing for a broader range of investment strategies.

Liquidity: Generally illiquid, with lock-in periods that may require investors to commit their capital for at least a year.Groww

Fee Structure: Typically employs a “2 and 20” model—2% management fee and 20% performance fee.

Pros:

Potential for high returns through aggressive and diverse investment strategies.

Cons:

High fees and limited liquidity.

Higher risk due to leveraged and speculative strategies.

Mutual Funds

Definition: Mutual funds are investment vehicles that pool money from multiple investors to purchase a diversified portfolio of stocks, bonds, or other securities. They are managed by professional fund managers.

Key Characteristics:

Investor Eligibility: Open to all investors, often with low minimum investment requirements.

Regulation: Highly regulated by authorities such as the U.S. Securities and Exchange Commission (SEC), ensuring transparency and investor protection.

Liquidity: Shares can be bought or sold at the fund’s net asset value (NAV) at the end of each trading day.

Fee Structure: Expenses include management fees and, in some cases, sales charges (loads).

Pros:

Professional management and diversification reduce individual investment risk.

Accessible to average investors with modest capital.

Cons:

Fees can erode returns over time.

Less control over individual investment choices.

Exchange-Traded Funds (ETFs)

Definition: ETFs are investment funds that hold a collection of assets and trade on stock exchanges like individual stocks. They combine features of both mutual funds and stocks.

Key Characteristics:

Investor Eligibility: Available to all investors, with shares purchasable through brokerage accounts.

Regulation: Subject to regulatory oversight similar to mutual funds, ensuring transparency.

Liquidity: Highly liquid; can be bought and sold throughout the trading day at market prices.

Fee Structure: Generally have lower expense ratios compared to mutual funds; however, brokerage commissions may apply.

Pros:

Flexibility to trade like stocks, including intraday trading and the use of limit orders.

Often more tax-efficient due to their unique structure.

Cons:

Prices can deviate from the NAV due to market fluctuations.

Some ETFs, especially those that are actively managed or specialized, may carry higher fees.

Comparative Overview

Aspect

Hedge Funds

Mutual Funds

ETFs

Investor Eligibility

Accredited investors with high minimum investments

Open to all investors with low minimum investments

Open to all investors through brokerage accounts

Regulation

Less regulated

Highly regulated

Regulated similarly to mutual funds

Liquidity

Limited, with lock-in periods

Daily liquidity at NAV

High liquidity; trades like stocks

Fee Structure

High fees (“2 and 20”)

Management fees and possible sales charges

Lower expense ratios; possible brokerage commissions

Investment Strategies

Diverse and complex, including leverage and derivatives

Primarily long-only strategies in stocks, bonds, and other securities

Tracks indices or sectors; can be passive or actively managed

Risk Profile

High risk due to aggressive strategies

Moderate risk, depending on fund objectives

Varies based on underlying assets and management style

Conclusion

Choosing between hedge funds, mutual funds, and ETFs depends on individual investment goals, risk tolerance, and financial capacity. Hedge funds offer the potential for high returns but come with significant risks and are accessible only to accredited investors. Mutual funds provide professional management and diversification, suitable for average investors seeking a balanced approach. ETFs offer flexibility, liquidity, and cost-efficiency, appealing to those who prefer a hands-on investment style. Understanding these differences enables investors to select the vehicle that best aligns with their financial objectives.

What Is Market Capitalization,and Why Does It Matter?

Understanding a company’s size and value is crucial for investors making informed decisions. One key metric that provides insight into these aspects is market capitalization. Let’s delve into what market capitalization is, how it’s calculated, its classifications, and why it holds significance in the investment world.

What Is Market Capitalization?

Market capitalization, often referred to as “market cap,” represents the total value of a company’s outstanding shares of stock. It’s a straightforward metric that gives investors an estimate of a company’s size and market value.

Calculation of Market Capitalization:

Market Capitalization=Share Price×Number of Outstanding SharesMarket Capitalization=Share Price×Number of Outstanding Shares

Example: If a company has 10 million shares outstanding, each priced at $50, its market capitalization would be: $50×10,000,000=$500,000,000$50×10,000,000=$500,000,000

Classifications Based on Market Capitalization

Companies are typically categorized into different groups based on their market capitalization:

Large-Cap: Companies with a market cap of $10 billion or more. These are often established firms with a significant market presence.

Mid-Cap: Companies with a market cap between $2 billion and $10 billion. They are usually in the process of expanding and have moderate risk profiles.

Small-Cap: Companies with a market cap between $300 million and $2 billion. These firms may offer higher growth potential but come with increased risk.

Micro-Cap: Companies with a market cap below $300 million. They are often newer or serve niche markets and can be highly volatile.

Why Does Market Capitalization Matter?

Understanding market capitalization is essential for several reasons:

Assessing Company Size and Stability: Market cap provides a quick snapshot of a company’s size, which can be indicative of its stability and maturity. Larger companies (large-cap) are generally more stable, while smaller companies (small-cap and micro-cap) might offer higher growth potential but with increased volatility.

Investment Strategy and Risk Assessment: Investors use market cap to align their portfolios with their risk tolerance and investment goals. For instance, a conservative investor might prefer large-cap stocks for their stability, whereas an aggressive investor might seek small-cap stocks for higher growth prospects.

Index Composition: Market capitalization influences the weighting of companies in major stock indices, such as the S&P 500. Companies with larger market caps have more influence on the index’s performance.

Valuation Insights: While market cap indicates the market’s valuation of a company, it doesn’t necessarily reflect its intrinsic value. Investors should consider other financial metrics and perform comprehensive analyses when making investment decisions.

Limitations of Market Capitalization

While market capitalization is a useful metric, it has its limitations:

Not a Comprehensive Measure of Value: Market cap reflects the market’s perception but doesn’t account for factors like debt, cash reserves, or the company’s overall financial health.

Market Volatility: Share prices, and consequently market cap, can be affected by short-term market fluctuations, which may not accurately represent a company’s long-term value.

Conclusion

Market capitalization is a fundamental metric that helps investors understand a company’s size and market value. By considering market cap alongside other financial indicators, investors can make more informed decisions and tailor their portfolios to align with their investment strategies and risk tolerance.

When it comes to understanding the economy, two critical concepts play a major role in shaping our financial lives: inflation and deflation. Both impact the value of money, the cost of goods, and overall economic stability. Let’s explore what they mean, how they affect your finances, and which one poses a greater risk.

What Is Inflation?

Inflation occurs when prices of goods and services rise over time, decreasing the purchasing power of money. A cup of coffee that cost $2 last year might cost $2.50 this year due to inflation. This gradual increase in prices is measured by the Consumer Price Index (CPI) and other economic indicators.

How Inflation Affects You

Cost of Living Increases: Essentials like groceries, housing, and transportation become more expensive.

Savings Lose Value: If your savings don’t grow at the same rate as inflation, your money loses purchasing power.

Investments Can Benefit: Assets like stocks and real estate often rise in value during inflationary periods, offering some protection.

Where to place a picture: A visual representation of inflation over time, showing the rising cost of goods (e.g., historical gas prices chart).

What Causes Inflation?

Demand-Pull Inflation: Increased demand for goods and services drives prices up.

Cost-Push Inflation: Rising production costs (like wages or raw materials) push prices higher.

Monetary Policy: When central banks print more money or keep interest rates low, inflation tends to rise.

What Is Deflation?

Deflation is the opposite of inflation—it occurs when prices of goods and services fall over time. While this might seem like a good thing, deflation can lead to economic slowdowns, lower wages, and decreased business profits.

How Deflation Affects You

Lower Prices: Consumers pay less for goods and services, making everyday purchases more affordable.

Job Losses: As businesses make less money, they may cut jobs, leading to higher unemployment.

Debt Becomes More Burdensome: Since money becomes more valuable, debts become harder to repay.

Where to place a picture: A graph comparing inflationary and deflationary periods in history, highlighting major economic downturns.

What Causes Deflation?

Decreased Consumer Demand: If people spend less, businesses lower prices to attract buyers.

Technological Advancements: Increased efficiency in production can drive prices down.

Tight Monetary Policy: High interest rates and reduced money supply can lead to deflation.

Inflation vs. Deflation: Which Is Worse?

Both inflation and deflation can harm the economy, but most economists agree that deflation is more dangerous in the long run. While moderate inflation (around 2%) is considered healthy, deflation can create a cycle of declining demand, job losses, and economic contraction.

How to Protect Your Money

During Inflation: Invest in assets that tend to appreciate (stocks, real estate, commodities). Consider inflation-protected bonds.

During Deflation: Hold onto cash or safe investments like government bonds, which may increase in value.

Where to place a picture: A side-by-side comparison chart of inflation vs. deflation, summarizing key effects on the economy.

Conclusion

Both inflation and deflation have major impacts on personal finance and the broader economy. While inflation erodes purchasing power, deflation can lead to economic stagnation. Understanding these forces can help you make informed financial decisions, whether it’s adjusting your investments, managing debt, or planning for the future.